The inconvenient truth: Australian coal is better in a net zero environment!

Despite the trend of a transition to renewable energy, the coal industry still plays a significant role in the global economy, yet Australian coal is not being acknowledged for its superior quality characteristics.

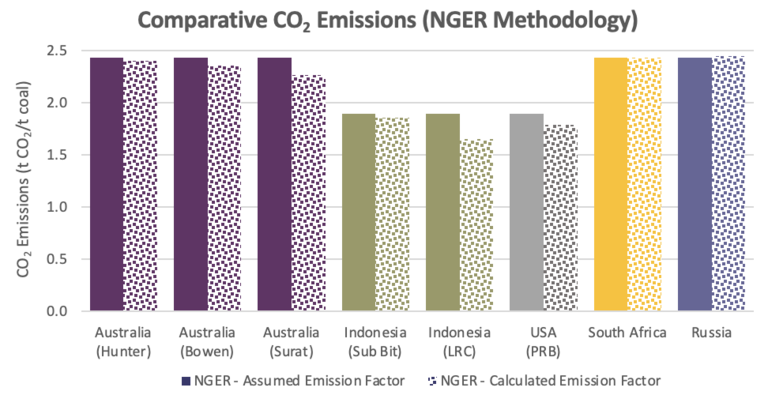

On the basis that reliable and affordable energy should never be politicised, we present an inconvenient truth – that increasing the production of Australian thermal coal is a far better outcome in a net zero environment. According to the Clean Energy Regulator and the National Greenhouse and Energy Reporting (NGER) Act, all coal mines should use a predefined energy content factor (i.e., 27 GJ/t for bituminous coal or 21 GJ/t for sub-bituminous coal) and a standard “assumed” carbon emission factor of 90 kg CO2‑e/GJ when calculating the impact of post-mining emissions (i.e., fuel combustion of coal).

Emissions calculated using NGER assumed emission factors are expressed as tonne CO2/tonne coal which misleadingly shows the more favourable performance of the lower rank (Indonesian and US) coals as shown below. A similar analysis has been made using the NGER calculated emission factor methodology to demonstrate that this does not take account of the properties of different coals, or their effect on power plant operations including CO2 emissions.

“These simple methods of calculating CO2 emissions have a disproportionate impact on the approval of expansion projects when environmental impacts seem to be the determining factor when approving or rejecting coal projects” says Dr Matthew Anderson, Director of Research and Consulting at Commodity Insights.

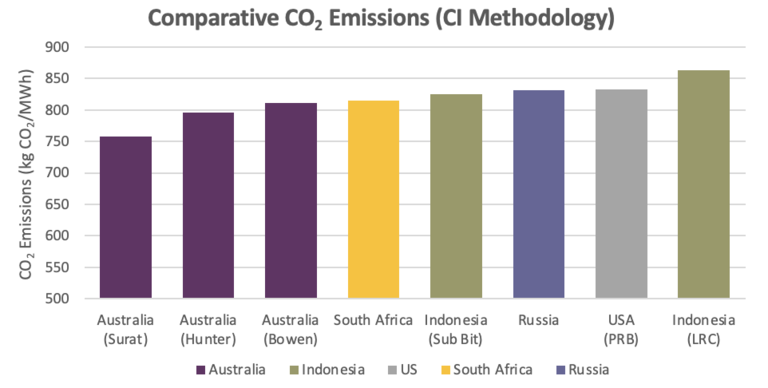

To demonstrate the impact of restricting or removing Australian thermal coal from the seaborne market, CO2 emissions resulting from the combustion of alternative thermal coals in a contemporary thermal power plant, have been calculated.

In addition to coal properties, the boiler efficiency associated with the combustion of each coal has been calculated as this impacts the required coal feed rate and CO2 emission levels. For the same electrical generation, the replacement of Australian thermal coal with coal from a different country would result in an increase in CO₂ emissions at the point of consumption (i.e., Scope 3 emissions). In the case of the Indonesian coal, this is largely due to reduced boiler efficiency resulting from the coal’s high moisture content, which, along with the coal’s lower calorific value, increases the coal feed rate required for the same electrical output.

Commodity Insights’ methodology differs from the National Greenhouse and Energy Reporting (NGER) methodology by calculating CO2 emissions from first principles and enables a more accurate analysis of the CO2 of the coal produced. This is equivalent to the Category 11 emissions definition¹ commonly referred to in Scope 3 frameworks to describe emissions at the point of consumption. This excludes Category 9 emissions from downstream transportation and distribution activities.

This shows that if an Australian thermal coal was replaced with sub-bituminous coal from Indonesia, an additional 37kg/MWh of CO2 emissions would be generated and an additional 75kg/MWh of CO2 emissions would be generated if low ranked coal (LRC) coal was used. Comparatively, replacement coal from Russia would result in an additional 43kg/MWh of CO2 emissions being generated. In other words, for every tonne of Australian thermal coal that is removed from the seaborne market, more CO2 will be emitted by being replaced with alternate thermal coals. This highlights that Australian thermal coal is less carbon intensive and would therefore result in significantly less CO2 emissions.

Commodity Insights has specialist technical capabilities that enables coal producers to accurately quantify their coal quality characteristics for investment and marketing purposes. Current and emerging producers are able to navigate complex commodity markets confidently with the right data and insights, including benchmarking and carbon implications to support operational and developmental requirements.

1Emissions from the end use of goods and services sold by the reporting company.