Don’t get too excited about lower European gas prices

Critically short on LNG import infrastructure, Europe’s ability to ramp up LNG imports is limited.

European gas prices continued to retreat in October from the astronomical highs of US$91/MMBtu in August, reaching US$10/MMBtu by the end of October. Unseasonably warm weather across Europe and the achievement of reaching the continent’s notional 80% storage capacity well ahead of the November deadline has prompted a ‘sigh of relief’ in government circles, but celebrating a mild winter in October (before winter arrives) would be premature, especially considering that the global energy complex is suffering from supply tightness amidst the ongoing conflict in Ukraine and the prospects of La Niña in the Asia-Pacific region.

Interestingly even the banking sector has jumped at the chance to downgrade forecasts, with the latest average forecast for the December 22 quarter now US$47/MMBtu, down from US$59/MMBtu previously. Forecasts for 2023 are also down around US$6/MMBtu on average, while prices for 2024 are now expected to average over US$13/MMBtu (compared to US$24/MMBtu previously), reflecting a growing belief that the European Union could avert an energy (supply) crisis this winter. While this is positive, Commodity Insights forecasts have not discounted the likelihood of further shocks to the European energy complex across winter and the potential repercussions that will emanate through global gas and coal markets.

European and Asian gas prices have historically been closely linked with Asia typically pricing at a US$2-3/MMBtu premium over Europe. However, at the time of writing a European price of US$10/MMbtu and an Asian price of US$30/MMBtu shows that European gas prices have trended back below Asian prices for the first time since April this year. This split indicates a market anomaly where European buyer behaviour pushed prices higher earlier while Asian buyers remain active in the market to build their winter inventories. We are watching this closely as a heavy winter draw down on Europe’s gas storage (or further sabotage of infrastructure) could swing European prices back to their historical alignment with Asian prices.

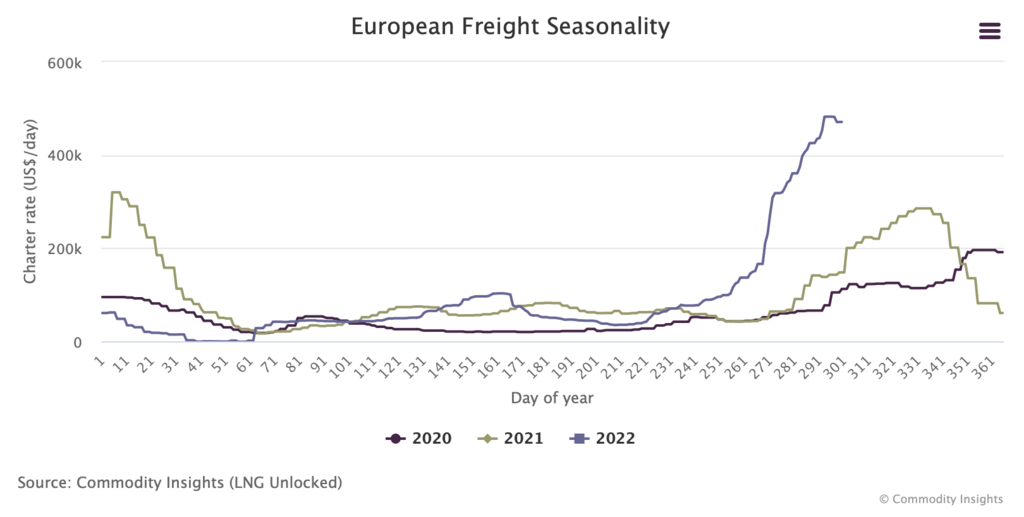

Supporting this thesis is the seasonally high LNG shipping rates into Europe which have now surged by 500% this year. The fact that shipping rates have so far not retreated at the same rate as European gas prices means that with mild weather, full storage, and limited connectivity across countries, infrastructure constraints will restrict the ramp up of gas imports. Consequently, this has led to a large number of LNG carriers (estimated to be over 35 at the time of writing) acting as floating storage while awaiting a berth to unload their cargos. At a charter rate of US$450,000/day, we estimate that the demurrage costs are likely to be US$15-20/MMBtu.

Meanwhile, thermal coal prices have eased marginally but still remain robust in the high US$300’s, as Europe builds its coal stocks for winter – previously this was hampered by low water levels on major rivers, preventing coal barges from proceeding inland. Coal remains cheaper than gas for power generation in North Asia based on spot prices, providing support in the short-mid-term. All eyes are watching the European winter to see what unfolds.