Can Mongolia replace Australia’s metallurgical coal supply to China?

As China grapples with a diplomatic ‘dispute’ with Australia, it is increasingly looking to source coal from its northern neighbour.

Since 2020, China has stepped up its efforts to engage with Mongolia to fill their coal shortage. A trade ‘dispute’ with Australia, the continued South China Sea shipping congestion, and a shortage of coal supply are testing the country’s economic capabilities and problem-solving skills.

In late 2020, Chinese state-owned companies were ordered to cease importing Australian coal, widely viewed as retaliation for Australia’s more critical stance on China. The restrictions on Australian coal presented a new opportunity for Mongolia to fill China’s coal shortfall. However, China has had a tumultuous relationship with Mongolia regarding access to the 7.5bt of coking coal estimated at Tavan Tolgoi spanning over the last decade.

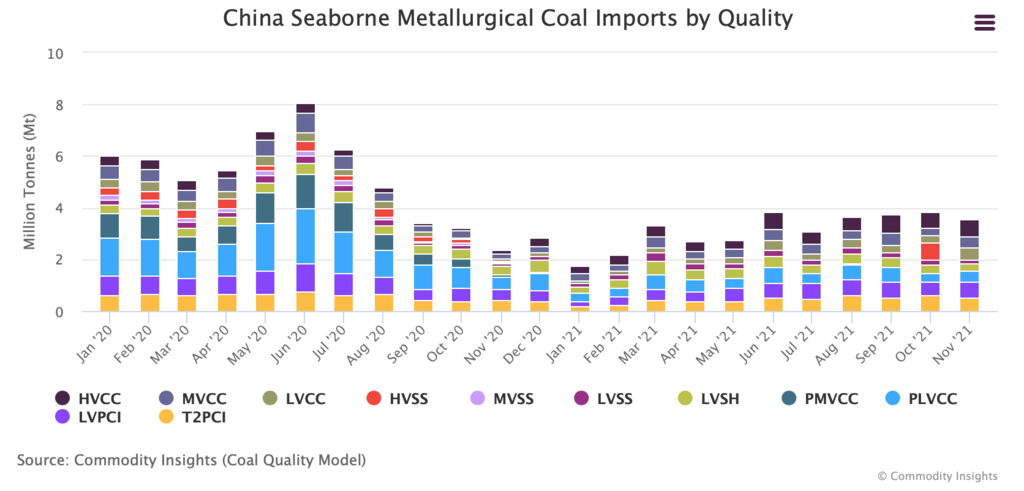

Mongolia, a major metallurgical coal exporter, already plays an integral part in China’s steel sector. In the past decade, Mongolia’s coal supply to China has grown from 21.3mt in 2011 to a high of 36.6Mt in 2019. In 2021, Mongolia exported 16.1Mt of coal to China, down from 28.7Mt in 2020 – nearly a 45% decrease following the closure of Gashuun Sukhait border station in the second half of 2021 due to increased COVID-19 cases in Mongolia.

While China is the major destination for Mongolia’s coking coal, notably by steel mills in Hebei province, its suitability to meet the needs of China’s heavy manufacturing industry is limited. The absence of high-quality Australian grades to blend [with other coal] reduces production efficiency in the steelmaking process, leading to lower profit margins. Accordingly, Mongolian coal has been a temporary solution for steel mills that rely on premium low-volatile Australian coking coal.

Australian premium hard coking coal has a number of sought-after attributes, including high coke strength after reaction, low sulphur and low ash, which only few exporters can offer.

Since the ban on Australia coal in late 2020, China has been forced to operate their steel mills on different specifications. With limited alternative import options (HVSS, PMVCC and PLVCC), quality concerns have forced steel mills to draw down on domestic coal supply because Russia, Canada and the US do not have the ability to provide both high volume and high quality coking coal.

Mongolia has the scale to replace some Australian coking coal by volume, but its lower quality does not make it a direct replacement. The absence of a suitable blend stock to replace the high-quality Australian coal may result in damage to the coke ovens at the major mills and ultimately the loss of steel-making capacity.

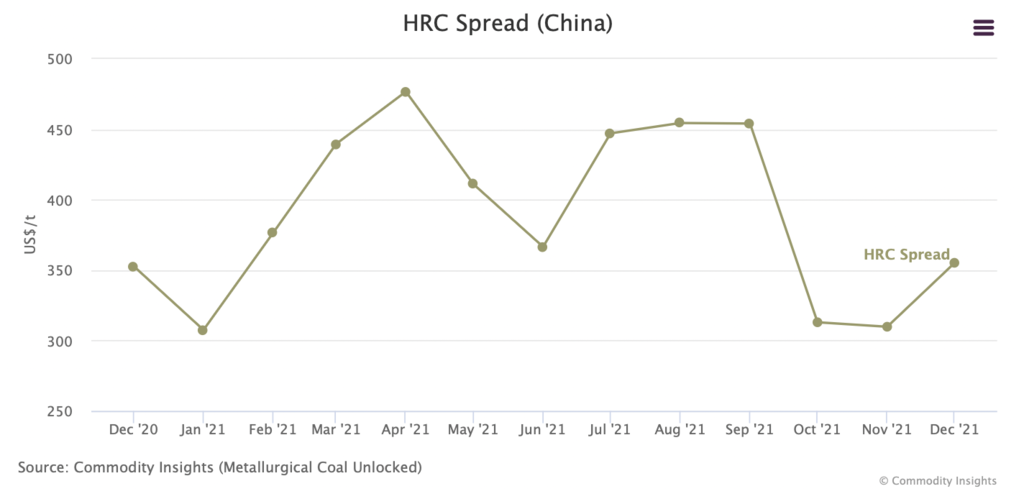

Furthermore, as the import price of coking coal delivered to China has risen to over US$600/t (MVCC/PMVCC), pushing Chinese steel makers up the cost curve and narrowing the HRC spread. This underlines the difficulties China faces trying to control commodity markets, which it has identified as a key risk to its economic recovery, and its foreign policy goals.

Although China is relatively self-sufficient in coking coal, with domestic mines supplying up to 80% of its needs, the scale of China’s steel industry means that it still needs to import over 65mtpa of the steelmaking ingredient. Thus China will find it increasingly difficult to diversify its supply of coking coal away from Australia indefinitely.

As for Mongolia, coal exports – and the mining industry at large – will continue to be the country’s primary source of revenue. Notwithstanding further covid supply risks, Mongolia will continue to promote its coal as a viable option for China.